When entering into a restaurant, I received a call from a Bank Executive. It could be a ‘Not Interested’ call but it was not actually. I was offered with low-cost Global Banking Account with Cross-Border money transfer in real time, any-time & any-where banking with high security, supporting & exchanging Cryptocurrency and Artificial Intelligence enabled Investment & Wealth Management suggestions on my portfolio. With captivating face, I wanted to know more about their services and planned to switch all my Banking and Investment Strategy with them.

Apparently, this kind of Banking Solutions are currently not available but there is a high chance of getting these revolutionary changes before the end of year 2020. How can I predict that? More than prediction, we can analyse and conclude the required transformation in Banking Industry by focusing on financial industry market movements. Let's take a look at the following facts which gave me guts to write about this topic.

Fact 1: 81% of Banking Industry CEOs are concerned about the speed of technological change

Fact 2: 76 Years took to adopt with Telephones but Smart phones have taken only 9 years

Fact 3: Approximately 10,000 FinTech Startups present around the globe focused on a particular innovative technology

Fact 4: Only 17% of Financial Firms feel that they are prepared to face the technological challenges

* Reference: PwC FS Tech 2020

These facts are from various genre but conveying a single statement to the Financial Industry.

"Change is Inevitable but Early Adoption is Necessary"

My intention of writing this article is not to explain about new technologies in Banking and Financial Sectors rather giving a heads-up to the readers to understand the future scope and necessity of technology migration in Financial Industry. Ok! Let's move further!

Fintech is the most popular & fancy term for Financial Technology used in Banking Sector and its supporting service providers. There are a lot of new initiatives happening in Fintech and Banks started to migrate from their legacy systems to the latest & advanced technical implementations. Already few global banks like J.P. Morgan Chase and HSBC Holdings have initiated to change their business process for adopting the cutting-edge technologies and advanced infrastructure.

Hybrid Clouds: It is a cloud computing infrastructure which uses a mix of on-premises or private cloud managed by the user and third-party or public cloud services between the two platforms for achieving common business goal. As per the analysis report of IBM Banking & Financial Markets, over 90% of enterprises will use multiple cloud services & platforms by 2020 and Financial Firms with a defined hybrid cloud strategy achieve 2.5x higher gross profits.

API Platforms: It is either a financial institution or independent service provider which leads to implement Open Banking infrastructure bringing many benefits for financial institutions like providing them with more opportunities to collaborate and partner with financial technologies. Here, two or more distinct but interdependent banks can transfer information through a programmatically consumable service or an Application Programming Interface (API).

Instant Payments: An electronic retail payment solution which is available 24/7/365 and resulting in the immediate or close-to-immediate interbank clearing of the transaction and crediting of the payee’s account with confirmation to the payer.

Robotic Process Automation: As per UiPath, RPA is the technology that allows anyone today to configure computer software or a “robot” to emulate and integrate the actions of a human interacting with digital systems to execute a business process. They also confirm that RPA robots are capable of mimicking many–if not most–human user actions. Banking and Financial Firms are continuously focusing on automating their Business Process to reduce the cost and improve the customer services.

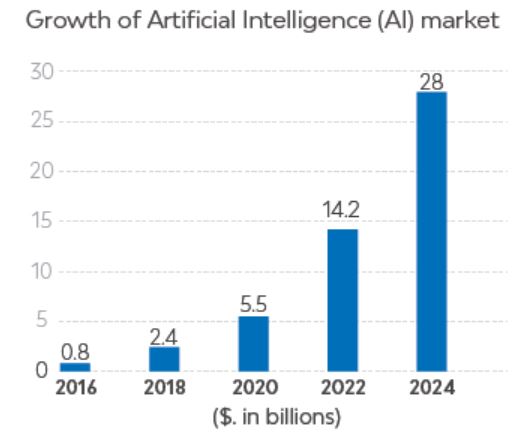

Artificial Intelligence: Problem of increasing automation is a fear of reduced loyalty due to less personal contact. But AI usage brings more personalized experience, in fact, banks are using AI to increase client satisfaction, improve efficiency and maintain customer loyalty in many ways. For example, ATMs can use face recognition using advanced features of AI and Deep Learning which helps to detect fraudulent activities.

Cyber-Security: Increasing digitalization in financial firms, Reserve Bank of India (RBI) has taken a step in the right direction by realizing the inherent need for banks to strengthen their cyber-security posture in the wake of the increasingly sophisticated nature and quantum of attacks. Major financial institutions are looking for a solution to accelerate threat detection and compliance with an all-in-one platform of essential security capabilities and seamlessly integrated threat intelligence to detect the latest threats.

Blockchain: According to a PwC report, 24% of financial executives from all around the world are very familiar with blockchain technology, with North Americans significantly more familiar than those from other regions. JP Morgan Chase and Bank of America have dedicatedly placed their faith in the future of Blockchain technology for Record Keeping, Security Markets, Smart Contracts and Cryptocurrency Exchanges.

Quantum Computing: JP Morgan Chase and Barclays are two of the biggest commercial members of Q-Network which is an advanced quantum computing development framework by IBM. Financial firms tap on the high-powered processing capabilities of quantum computing and optimize for big data analytics, portfolio analysis, asset appraisal, and high-frequency trading.

Smart Machines: Smart machines offer huge potential benefits to early adopters within financial services, even with regulators barring banks from some use cases. Most banks will invest in the six main types of smart machines in 2020. They are Smart Vision Systems, Virtual Customer Assistants, Virtual Personal Assistants, Smart Advisors, NLP Technology and Smart Campus Infrastructure.

Backlogs & Priorities

Things are not going as per financial firm's implementation plan. Challenges are increasing because of dynamic growth in technology innovations and customer's expectation. In a recent Deloitte poll, just 10% of the respondents said their banks are in a state of "being digital", with another 22% only "becoming digital". Technology is almost ready to go-live especially in Instant Payments, Open Banking and Hybrid Clouds for Banking Sector but many financial firms are living with their existing systems.

What about customers? Based on a global survey, Accenture found that 31% of bank customers would consider Google, Amazon or Facebook to provide Banking Solutions. Reason is simple, Yes, it is very simple. Bank Customers expect that Banking must be simple, easily accessible, 24x7 available, extremely secure, user friendly and suggestible. As I mentioned earlier, in financial sector, early adopters will secure their valuable clients and portfolios. So, the following are the top priorities of Banking and Financial firms to compete with Year-2020.

1. Updating Business Process and Information Technology Operational Models

2. Adopting Digital-Labor (Bot) and Artificial Intelligence

3. Improving intelligence to know your customer needs

4. Connecting Anything from Anywhere with cyber-security

5. Hiring Talented and Skilled Executives to utilize all technologies

Information Technology Radar

IT firms consider on disruptive banking technologies such as Blockchain, AI & Bot and Open Banking as strong priority items. Consulting firms are mainly focusing on transforming existing operations of their banking clients towards the digital ecosystem. Many Technology and Consulting companies started investing on Start-ups because new innovations & disruptions in the banking and financial industry make the future look very exciting and technology focused.

Let's look at some interesting investment plans on new technology

Key Takeaways

1. Gap between current financial systems and technology development is very high

2. Banks are ready to continuously upgrade disruptive technological solutions

3. FinTech Start-ups play major role on Banking and Financial Service innovations

4. Need of IT Vendors with excellent innovation portfolio is increasingly high

5. Demand is created for dynamic and skilled financial and IT consultants

Thanks for your time! Post your queries and suggestion and I will try to respond you as early as possible. Have a wonderful day!

Disclaimer: Information provided in this article are my understanding being shared for the educational & knowledge purposes only. All the information provided here is from public domain, to best of my knowledge no proprietary information is used. If any questions or concerns about the content, please contact me directly.